India can absorb energy shock but fiscal strains possible: S&P

15-04-2026 12:00:00 AM

Oil Shock Impact | Economic growth could slow by up to 80 basis points

New Delhi

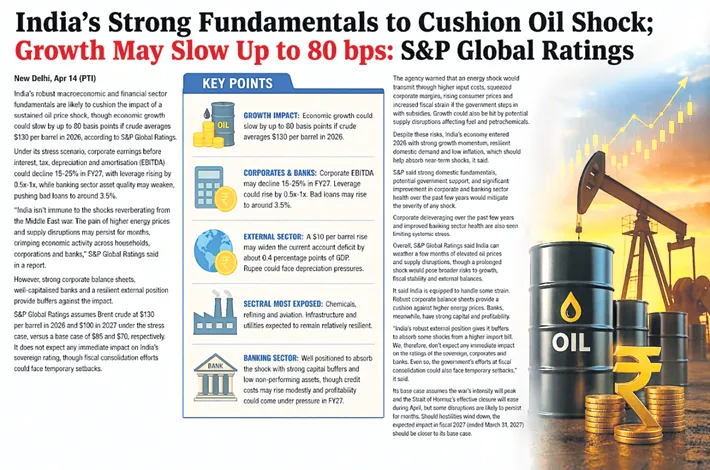

India's robust macroeconomic and financial sector fundamentals are likely to cushion the impact of a sustained oil price shock, though economic growth could slow by up to 80 basis points if crude averages $130 per barrel in 2026, according to S&P Global Ratings.

Under its stress scenario, corporate earnings before interest, tax, depreciation and amortisation (EBITDA) could decline 15%–25% in FY27, with leverage rising by 0.5x–1x, while banking sector asset quality may weaken, pushing bad loans to around 3.5%.

"India isn't immune to the shocks reverberating from the Middle East war. The pain of higher energy prices and supply disruptions may persist for months, crimping economic activity across households, corporations, and banks," S&P Global Ratings said in a report.

However, strong corporate balance sheets, well-capitalised banks and a resilient external position provide buffers against the impact.

The rating agency assumes Brent crude at $130 per barrel in 2026 and $100 in 2027 under the stress case, versus a base case of $85 and $70, respectively. It does not expect any immediate impact on India's sovereign rating, though fiscal consolidation efforts could face temporary setbacks.

Higher oil prices could widen the current account deficit, with estimates suggesting a $10 per barrel increase may expand the gap by about 0.4 percentage points of GDP. The rupee could also face depreciation pressures amid risk-off sentiment and a rising import bill.

S&P Global Ratings warned that an energy shock would transmit through higher input costs, squeezed corporate margins, rising consumer prices and increased fiscal strain if the government steps in with subsidies. Growth could also be hit by potential supply disruptions affecting fuel and petrochemicals.

Despite these risks, India's economy entered 2026 with strong growth momentum, resilient domestic demand and low inflation, which should help absorb near-term shocks. Strong domestic fundamentals, potential government support, and significant improvement in corporate and banking sector health over the past few years would mitigate the severity of any shock.

While sectors such as chemicals, refining and aviation are most exposed, infrastructure and utilities are expected to remain relatively resilient. Corporate deleveraging over the past few years and improved banking sector health are also seen limiting systemic stress. Indian banks are well positioned to absorb the shock, supported by strong capital buffers and low non-performing assets, though credit costs may rise modestly, and profitability could come under pressure in FY27.