Power pivot, energy alliances fracture, winners emerge

04-05-2026 12:00:00 AM

STRATEGIC MOMENT BECKONS INDIA| Supply decentralisation and shifting invoicing norms alter pricing dynamics, strengthening national bargaining power and insulating external balances sustainably

Election results and likely fuel price hikes amid crude surge could test households, yet India’s strategy may cushion near-term impact

Palazhi Ashok Kumar MUMBAI

In an age defined by noise, the most consequential shifts often arrive in silence. Beneath the visible tremors of conflict in West Asia and the sharp oscillations of crude benchmarks, a deeper realignment is unfolding—one that may yet redraw the architecture of energy power and, with it, the economic destiny of nations.

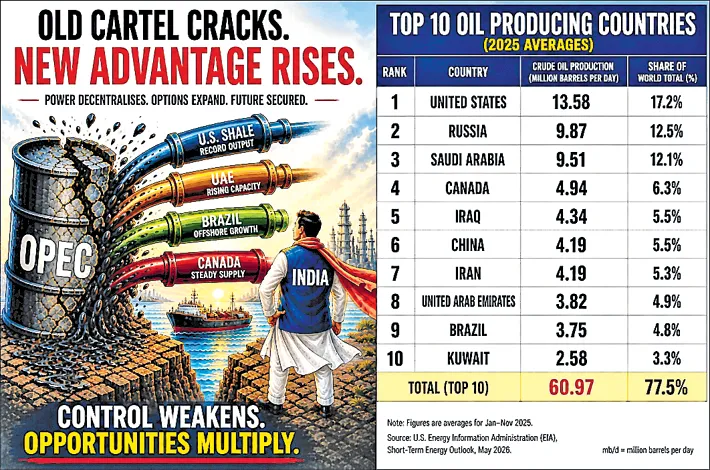

For decades, the global oil market moved to a disciplined rhythm orchestrated by the OPEC and its extended alliance. Coordinated supply restraint ensured price stability—at a cost. Import-dependent economies, India foremost among them, paid a premium not merely in currency, but in constrained policy freedom.

That era is beginning to loosen—subtly, but decisively. The notion of a unified producer front is under visible strain. Divergent national priorities—production ambitions, fiscal compulsions, geopolitical alignments—are diluting the cartel’s once formidable cohesion.

The UAE, producing around 3.8–4.0 mb/d and targeting 5 mb/d by 2027, reflects a broader shift toward sovereign flexibility. This autonomy introduces competitive supply impulses into a market long governed by coordinated restraint. Simultaneously, non-OPEC producers continue to assert structural influence. The United States leads global output at roughly 13.5–13.7 mb/d, while Canada (4.9 mb/d) and Brazil (3.7–3.8 mb/d) deepen supply diversity. Russia and Saudi Arabia continue calibrated production within the 9–10 mb/d range, reinforcing a system shifting from control to competition. For India, the present moment remains demanding. Brent crude surged beyond $125 per barrel in April 2026, before easing toward $110–115—levels that still strain inflation, fiscal balances and the rupee, which has tested the ₹94–95 band.

Politics, inevitably, intersects with pricing power. As counting begins today (May 4) across five key states/UT, policymakers face a delicate balance. Closed-door assessments suggest modest retail increases—petrol and diesel by ₹4–5 per litre, LPG by ₹40–50—may follow global crude spikes. While politically sensitive, such moves could prove temporary if incoming supply from the UAE and other partners stabilises domestic availability. Yet within this pressure lies strategic possibility.

A significant diplomatic signal is imminent, as Prime Minister Narendra Modi is scheduled for a mid-May visit to the UAE, reinforcing a partnership that has evolved into strategic alignment. In a region shaped by volatility, this engagement signals intent—towards stability, diversification and long-term assurance.

Parallel to this geopolitical recalibration is the gradual emergence of alternative settlement frameworks. Bilateral energy trade in local currencies—particularly between India and the UAE—is gaining traction. Such a shift could reduce dollar dependence, moderate exchange volatility, and enhance monetary autonomy. Markets remain divided. Some institutions project crude easing toward $75–80 by the latter part of the decade, while others warn of sustained volatility. Both views reflect a system in transition.

The future of energy will not be defined solely by abundance or scarcity, but by access, adaptability and alignment. Strategic petroleum reserves must deepen. Financial architecture must evolve to support diversified invoicing frameworks. Above all, macroeconomic policy must remain anchored in credibility.