India’s NBFCs enter a new oil shock phase

02-05-2026 12:00:00 AM

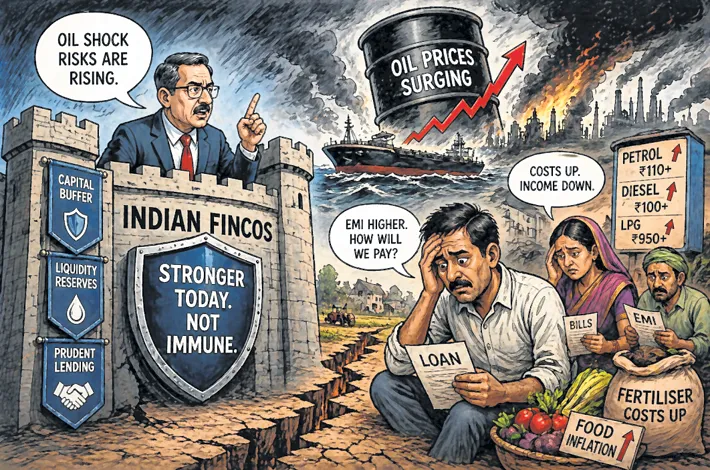

FRAGILITY BENEATH STRENGTH. Credit Under Siege | Households, MSMEs, and farmers face mounting stress as inflation bites, testing the resilience of the country's shadow banking sector

S&P Global Ratings outlines downside case where Brent approaches $130, amplifying volatility, funding stress, and systemic vulnerabilities across credit markets

Palazhi Ashok Kumar MUMBAI

India’s vast shadow banking network is staring at a gathering storm, as war-driven oil shocks ripple through the economy, threatening to expose hidden fractures beneath years of carefully built financial resilience.

A sharply worded assessment by S&P Global Ratings on Friday warns that while India’s non-bank finance companies (NBFCs) appear well-capitalised on the surface, a prolonged surge in energy prices could trigger a chain reaction—weakening borrowers, tightening liquidity and ultimately testing the system’s endurance.

At the heart of the risk lies oil. Disruptions in the Strait of Hormuz—artery to nearly a third of global crude flows—have already unsettled markets. S&P’s base case assumes partial normalisation by late May. But in a darker scenario, Brent crude could surge to an average $130 a barrel in 2026, unleashing sustained pressure across credit markets.

The tremors would be felt first by borrowers. Micro, small and medium enterprises, already operating on thin margins, face rising input costs and shrinking cash flows, sources at S&P told The FPJ Money.

As repayment capacity erodes, delinquency risks could climb, feeding stress directly into lenders’ balance sheets. Households are no less exposed. Higher fuel and food costs are steadily draining disposable incomes, with early warning signs expected in unsecured retail loans, microfinance and commercial vehicle financing. While relatively safer segments such as housing and gold-backed loans provide a buffer, they are unlikely to fully offset broader stress if inflation persists. Rural India presents a parallel fault line. Elevated natural gas prices are inflating fertiliser costs, threatening farm economics and liquidity cycles.

Although inventories remain adequate for now, a prolonged disruption could tighten supplies and strain the next sowing season, amplifying risks across agricultural lending. S&P, however, said the energy price shock won’t last forever and that NBFCs should generally be able to withstand the stress. Policy intervention may offer temporary relief. Subsidies, targeted credit guarantees and potential regulatory forbearance from the RBI could help contain immediate fallout. Yet such measures carry their own risks—delaying the recognition of stress rather than resolving it. More critically, fincos remain uniquely exposed to shifts in market sentiment. Unlike banks, their dependence on wholesale funding leaves them vulnerable to sudden liquidity squeezes.

For now, ratings remain broadly stable. But the warning is unmistakable: resilience has limits. If oil prices remain elevated and geopolitical tensions persist, India’s credit ecosystem could face a slow-burning crisis—one that begins quietly in borrower balance sheets, but risks escalating into a broader financial strain.